Last week was one heckuva week for societal problems related to race relations. Seems like someone turned over a rock and the 1950s crawled out. We started with Cliven Bundy, the Nevada rancher who has been using federal property (read our land) for grazing his cattle for 20 years without paying for it, said after the armed confrontation with federal officials, that “I wonder if Negros weren’t better off as slaves.” But he says he is not a racist, but wow. That’s right up there with Rush Limbaugh’s comments about Native Americans in his book 15 years ago.

Then we had newspaper columnist and right-wing wonk, Thomas Sowell, who is black, saying in a recent column that “you are poor because you don’t work.” And it is your fault you don’t work. In “higher income families, people work.” So using that line of racist nonsense, given that minorities are disproportionately un- or under-employed, does Mr. Sowell really believe that it is really the choice of all of these people not to work?! Could there be any other causal links like the lack of education, decaying infrastructure or the lack of local opportunities in their community that might just come into play? That’s like saying Detroit’s problem is not the lack of job opportunities, but the fact that no one wants to work in Detroit. I think not.

The we have Donald Sterling, the owner of the Los Angeles Clippers NBA team, who was taped making racists comments, then received a lifetime ban and multi-million dollar fine for his comments about minorities, and then, instead of apologizing, states that he wishes he’d just paid the woman who taped him off. Huh? Of course it is not the first time for Mr. Sterling who lost a case several years ago over his practices of renting property in LA, so I guess we should have expected it.

Of course there are those who argue these folks were simply misunderstood. Maybe Mr. Sowell was just pandering to his fan base, but what does that say about his fan base that he can write a column that purports that “you are poor because you don’t work” because you don’t want to work and no one says anything? He clearly appears to be besmirching the inner city minority population, but as I noted in a prior blog, rural America is significantly worse off economically than urban America. Rural America is where health care suffers, the lack of health insurance is pervasive, income are lower and unemployment higher. There are poor across all races, and in all settings. And given his fan base is includes a lot of poor, white, rural people who aren’t making a lot of money or who can’t find jobs, he’s talking about you!

The Bundy comments stem from his standoff with federal officials over many years of not paying for grazing (like the rest of us could get away with that!). He and those that came armed to his defense are more indicative of a larger, far-right, anti-government sentiment around the country that has persisted for years. The west has a number of these groups (recall Ruby Ridge, Waco, Black Hawk helicopter-ists, etc.) that are basically anarchists that disagree with America as it is today. All white. But of course as we have seen in the Sudan, Rwanda, the middle east and throughout history, hate can come from all races and religions. All harboring hatred of others not like them. Understanding why is more difficult, but the commonality seems to be that they all have the perception that the others are somehow treated differently, which allows them to move up the economic ladder faster or allows them to “game the system.” The perception, which may be completely false, persists because it somehow justifies the actions of these people.

So given the comments of the past week, are we back in the 1950s? Or 1870s? How are we here in 2014? Prejudice and hate were not wiped away magically by civil rights legislation, integration, communication and education alone, but really, does this type of attitude have a place in today’s world? If so why? Hate has created trouble in the world for thousands of years. Hate is a problem because hate is a means to distract people from real problems or to force your problems on others. But in truth, psychologists will tell you that in most cases, the Haters tend to hate themselves, which is something we all need to remember. Hate is developed because you cannot control a situation or someone else gets something you want. Therefore it is that someone else’s fault, not yours. It is easier when race, sex, sexual orientation, religion or other factors represent the “somebody else,” but the reality is haters hate themselves first, then project their hate onto others. They need help. Professional help. Counseling. Many of them. Even whole societies. They need to go get help for themselves and the rest of us.

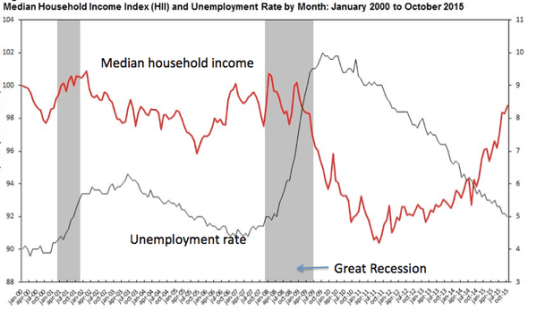

One of the issues I always include in rate studies is a comparison of water rates with other basic services. Water always comes in at the bottom. But that works when everyone has access and uses those services. Several years ago a study indicated that cable tv was in 87-91 % of home. At the time I was one of the missing percentage, so I thought it was interesting. However, post the 2008 recession, and in certain communities, this may be a misplace comparison. A recent study by Emmanuel Saez and Gabriel Zucman notes that the top 0.1% have assets that are worth the same as the bottom 90% of the population! Yes, you read that correctly. Occupy Wall Street had it wrong. It’s not the 1% it is the 0.1%. This is what things were like in the 1920s, just before the Great Depression. The picture improved after the implementation of tax policies (the top tax rate until 1964 was 90% – yes you read that right – 90%). Then the tax rate was slowly reduced to deal with inflation. The picture continued to improve until supply side economics was introduced in the early 1980s when the disparity started to rise again (see their figure below), tripling since the late 1970s (you recall the idea was give wealthy people more money and they would invest it in jobs that would increase employment opportunities and good jobs for all, or something like that). Supply side economics did not/does not work (jobs went overseas), and easy credit borrowing and education costs have contributed to the loss of asset value for the middle class as they strove to meet job skills requirements for better jobs. In addition wages have stagnated or fallen while the 0.1% has seen their incomes rise. The problem has been exacerbated since 2008 as they report no recovery in the wealth of the middle class and the poor. So going back to my first observation – what gets cut from their budget, especially the poor and those of fixed pensions? Food? Medicine? Health care? My buddy Mario (86 year old), still works because he can’t pay his bills on social security. And he does not live extravagantly. So do they forego cable and cell phones? If so the comparison to these costs in rate studies does not comport any longer. It places at risk people more at risk. And since, rural communities have a lower income and education rate than urban areas, how much more at risk are they? This is sure to prove more interesting in the coming years. Hopefully with some tools we are developing, these smaller communities can be helped toward financial and asset sustainability. But it may require some tough decisions today.

One of the issues I always include in rate studies is a comparison of water rates with other basic services. Water always comes in at the bottom. But that works when everyone has access and uses those services. Several years ago a study indicated that cable tv was in 87-91 % of home. At the time I was one of the missing percentage, so I thought it was interesting. However, post the 2008 recession, and in certain communities, this may be a misplace comparison. A recent study by Emmanuel Saez and Gabriel Zucman notes that the top 0.1% have assets that are worth the same as the bottom 90% of the population! Yes, you read that correctly. Occupy Wall Street had it wrong. It’s not the 1% it is the 0.1%. This is what things were like in the 1920s, just before the Great Depression. The picture improved after the implementation of tax policies (the top tax rate until 1964 was 90% – yes you read that right – 90%). Then the tax rate was slowly reduced to deal with inflation. The picture continued to improve until supply side economics was introduced in the early 1980s when the disparity started to rise again (see their figure below), tripling since the late 1970s (you recall the idea was give wealthy people more money and they would invest it in jobs that would increase employment opportunities and good jobs for all, or something like that). Supply side economics did not/does not work (jobs went overseas), and easy credit borrowing and education costs have contributed to the loss of asset value for the middle class as they strove to meet job skills requirements for better jobs. In addition wages have stagnated or fallen while the 0.1% has seen their incomes rise. The problem has been exacerbated since 2008 as they report no recovery in the wealth of the middle class and the poor. So going back to my first observation – what gets cut from their budget, especially the poor and those of fixed pensions? Food? Medicine? Health care? My buddy Mario (86 year old), still works because he can’t pay his bills on social security. And he does not live extravagantly. So do they forego cable and cell phones? If so the comparison to these costs in rate studies does not comport any longer. It places at risk people more at risk. And since, rural communities have a lower income and education rate than urban areas, how much more at risk are they? This is sure to prove more interesting in the coming years. Hopefully with some tools we are developing, these smaller communities can be helped toward financial and asset sustainability. But it may require some tough decisions today.