The true risk to the community of pipe damage is underestimated and the potential for economic disruption increases. The question is how do we lead our customers to investing in their/our future? That is the question as the next 20 years play out. Making useful assumptions about increases in demands, prices, inflation rates etc. are key to useful projections and long-term sustainability. Building too much or too little capacity for example can have disastrous consequences (to the ratepayers on the former, to the local economy for the latter).

Getting funding relies on economic strength, a problem of you are in a depressed area (Detroit) or a boom that could crash at any time (North Dakota). P3 opportunities are available for cash strapped communities but they come with a cost. Risk must be allocated fairly – the private community will not take on too much risk without increasing costs significantly. Loss of control is one of those risk conversion issues. Extensive planning and feasibility analyses should be expected – far more scrutiny than most utilities are used to. The economic strength of the community is important to private investors.

In a prior blog we talked about the boom towns of North Dakota. Things were booming in 2013 but the downturn in oil prices may get ugly. The need for more fracking wells may have decreased (at least temporarily) and the decrease in the oil and gas costs has cut into local revenues, so is this is the time to keep planning for the boom? South Florida did this in the early 2000s – and well, that real estate boom put quite a dent in the economy and population estimates for 2020 and 2030. The balloon popped and so did the economy. South Florida had the resiliency to bounce back because of weather and proximity to South America. We have seen the result to an industrial economy – where a community relies on industry, well industry can be fickle. Ask Detroit. Or Cleveland. Or any number of other Rust Belt cities. Now they have infrastructure, but much of it is underused.

So while the Plains states plan for the boom, the boom has settled in some places. Already the oil and gas industry has shed 100,000 jobs (many high salary). Texas, Kansas, North Dakota and Oklahoma are facing financial challenges in 2015 due to funding losses. Alaska is dipping into reserves. But that doesn’t mean the results of the 2010-2014 boom are not continuing, or at least portions of them. Frack water continues to be discharged to local wastewater systems, but the revenues to pay for the needed upgrades is lacking. Effluent limits for nitrogen and TOC for some rivers have decreased as a result of constant increased loading to the streams (more flow increases total loads, so if flows remain the same, the concentrations must decrease to maintain total loading). The costs to reduce ammonia, for example from 10 mg/l to 2 or 3 mg/L can be $1-2/1000 gallon – over 50% or more of the current cost for treatment.

So is it a surprise that some communities fight the boom times? Booms create disruption and uncertainly, and a need for technology (and costs). Maybe stability does matter, as it can contain costs and treatment requirements. However the boom can help communities in financial distress. Detroit and Flint would love a boom – both have the infrastructure in place to support it as opposed to rural communities in the Plains. But that’s is a key – they already HAVE the infrastructure in place. The Plains, well, do not.

There is a lot of older, underutilized infrastructure out there. Detroit, Flint, Cleveland, Akron, Toledo and Philadelphia are among the older industrial cities that have stable populations – people that live there most of their lives, have a trained and educated workforce, and normally have lots of water and infrastructure, and lots of potential employees, all of which are underutilized and at risk due to economic losses. But the booms rarely go to older cities. How that is? Is this a leadership issue? Convenience? Quick profits? And how long will the boom last? Is it a matter of lack of understanding or regulations that creates the boom? A combination of factors? A better PR program?

Remember we all play defense. Industry does not. Industry plays offense all the time. The private sector mode is play offense. Get the message out. Frame the message. Win the game. Is winning the game at any cost the right answer? For boomers it is. What about the rest of us?

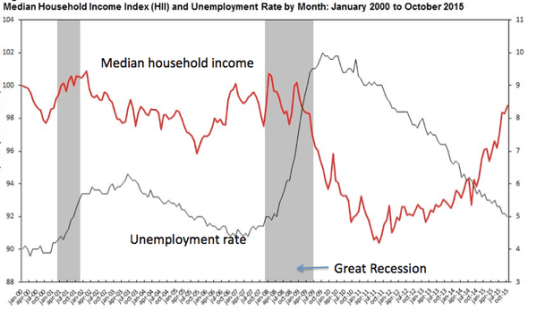

One of the issues I always include in rate studies is a comparison of water rates with other basic services. Water always comes in at the bottom. But that works when everyone has access and uses those services. Several years ago a study indicated that cable tv was in 87-91 % of home. At the time I was one of the missing percentage, so I thought it was interesting. However, post the 2008 recession, and in certain communities, this may be a misplace comparison. A recent study by Emmanuel Saez and Gabriel Zucman notes that the top 0.1% have assets that are worth the same as the bottom 90% of the population! Yes, you read that correctly. Occupy Wall Street had it wrong. It’s not the 1% it is the 0.1%. This is what things were like in the 1920s, just before the Great Depression. The picture improved after the implementation of tax policies (the top tax rate until 1964 was 90% – yes you read that right – 90%). Then the tax rate was slowly reduced to deal with inflation. The picture continued to improve until supply side economics was introduced in the early 1980s when the disparity started to rise again (see their figure below), tripling since the late 1970s (you recall the idea was give wealthy people more money and they would invest it in jobs that would increase employment opportunities and good jobs for all, or something like that). Supply side economics did not/does not work (jobs went overseas), and easy credit borrowing and education costs have contributed to the loss of asset value for the middle class as they strove to meet job skills requirements for better jobs. In addition wages have stagnated or fallen while the 0.1% has seen their incomes rise. The problem has been exacerbated since 2008 as they report no recovery in the wealth of the middle class and the poor. So going back to my first observation – what gets cut from their budget, especially the poor and those of fixed pensions? Food? Medicine? Health care? My buddy Mario (86 year old), still works because he can’t pay his bills on social security. And he does not live extravagantly. So do they forego cable and cell phones? If so the comparison to these costs in rate studies does not comport any longer. It places at risk people more at risk. And since, rural communities have a lower income and education rate than urban areas, how much more at risk are they? This is sure to prove more interesting in the coming years. Hopefully with some tools we are developing, these smaller communities can be helped toward financial and asset sustainability. But it may require some tough decisions today.

One of the issues I always include in rate studies is a comparison of water rates with other basic services. Water always comes in at the bottom. But that works when everyone has access and uses those services. Several years ago a study indicated that cable tv was in 87-91 % of home. At the time I was one of the missing percentage, so I thought it was interesting. However, post the 2008 recession, and in certain communities, this may be a misplace comparison. A recent study by Emmanuel Saez and Gabriel Zucman notes that the top 0.1% have assets that are worth the same as the bottom 90% of the population! Yes, you read that correctly. Occupy Wall Street had it wrong. It’s not the 1% it is the 0.1%. This is what things were like in the 1920s, just before the Great Depression. The picture improved after the implementation of tax policies (the top tax rate until 1964 was 90% – yes you read that right – 90%). Then the tax rate was slowly reduced to deal with inflation. The picture continued to improve until supply side economics was introduced in the early 1980s when the disparity started to rise again (see their figure below), tripling since the late 1970s (you recall the idea was give wealthy people more money and they would invest it in jobs that would increase employment opportunities and good jobs for all, or something like that). Supply side economics did not/does not work (jobs went overseas), and easy credit borrowing and education costs have contributed to the loss of asset value for the middle class as they strove to meet job skills requirements for better jobs. In addition wages have stagnated or fallen while the 0.1% has seen their incomes rise. The problem has been exacerbated since 2008 as they report no recovery in the wealth of the middle class and the poor. So going back to my first observation – what gets cut from their budget, especially the poor and those of fixed pensions? Food? Medicine? Health care? My buddy Mario (86 year old), still works because he can’t pay his bills on social security. And he does not live extravagantly. So do they forego cable and cell phones? If so the comparison to these costs in rate studies does not comport any longer. It places at risk people more at risk. And since, rural communities have a lower income and education rate than urban areas, how much more at risk are they? This is sure to prove more interesting in the coming years. Hopefully with some tools we are developing, these smaller communities can be helped toward financial and asset sustainability. But it may require some tough decisions today.